China GDP grows 5% in Q1, beats expectations on exports, spending strength

Introduction & Market Context

Itaú Unibanco Holding S.A. (NYSE:ITUB) released its fourth quarter 2025 results on February 5, 2026, showcasing strong growth in local currency terms while falling short of USD-based analyst expectations. Despite missing forecasts, the bank’s shares rose 1.88% in premarket trading to $8.65, reflecting investor confidence in the company’s long-term strategy and robust dividend policy.

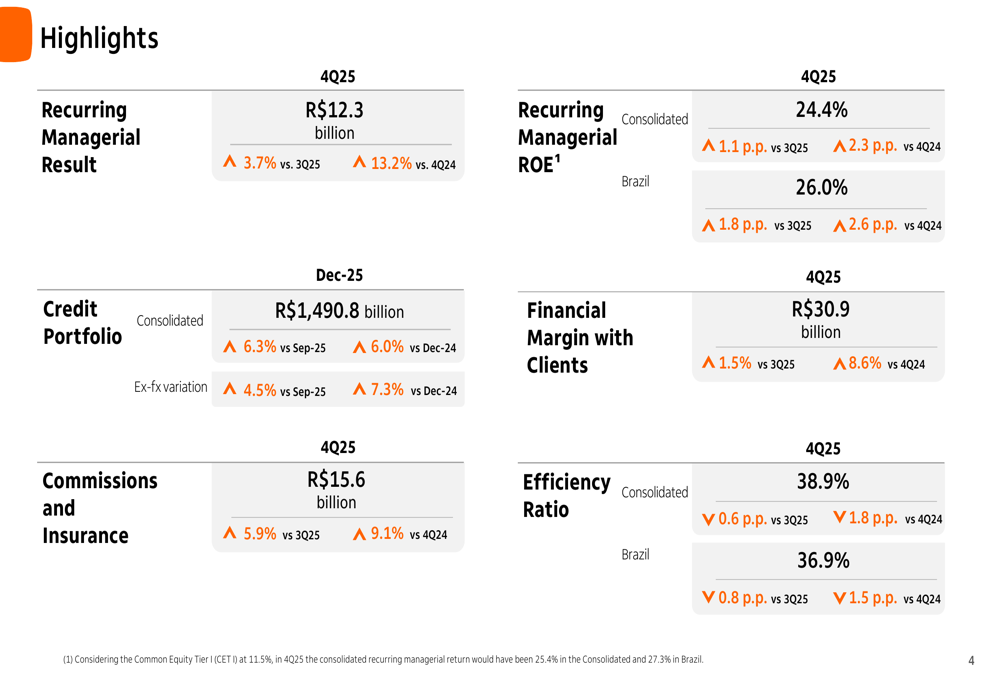

The Brazilian banking giant reported a recurring managerial result of R$12.3 billion (approximately $2.25 billion), representing a 3.7% increase compared to the previous quarter and a 13.2% rise year-over-year. However, when converted to USD, these results translated to earnings per share of $0.1924, missing analyst expectations of $0.2025 by 4.99%.

Quarterly Performance Highlights

Itaú’s fourth quarter performance demonstrated solid momentum across key metrics in local currency terms. The bank achieved a consolidated recurring ROE of 24.4% (26.0% in Brazil), improving by 1.1 percentage points quarter-over-quarter and 2.3 percentage points year-over-year.

As shown in the following quarterly highlights chart:

The bank’s credit portfolio reached R$1,490.8 billion, growing 6.3% compared to September 2025 and 6.0% year-over-year. Financial margin with clients increased to R$30.9 billion, up 1.5% quarter-over-quarter and 8.6% compared to Q4 2024. Commission and insurance revenue showed strong growth at R$15.6 billion, rising 5.9% from the previous quarter and 9.1% year-over-year.

Efficiency continued to improve, with the consolidated efficiency ratio reaching 38.9% (36.9% in Brazil), representing improvements of 0.6 and 0.8 percentage points respectively compared to the previous quarter.

Strategic Evolution & Long-term Performance

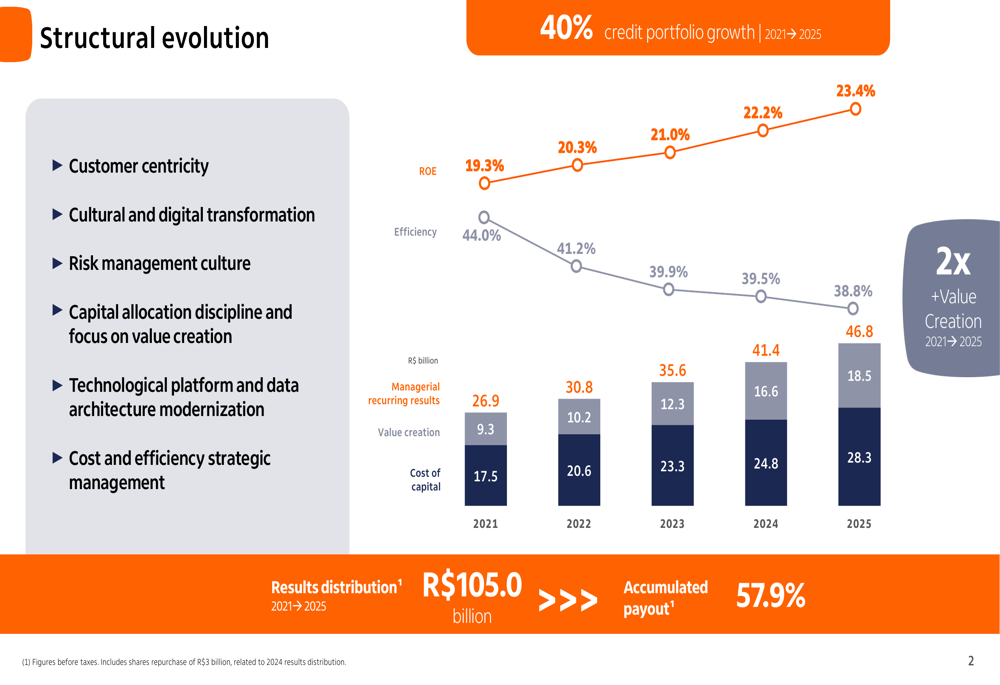

The presentation highlighted Itaú’s strategic evolution from 2021 to 2025, focusing on customer centricity, digital transformation, risk management culture, and capital allocation discipline. These initiatives have driven significant improvements in key performance indicators.

The following chart illustrates the bank’s structural evolution and results over this period:

ROE improved from 18.5% in 2021 to 23.4% in 2025, while efficiency strengthened from 45.1% to 38.8% during the same period. The credit portfolio expanded by 40% between 2021 and 2025, and the bank distributed R$105.0 billion to shareholders with an accumulated payout of 57.9%.

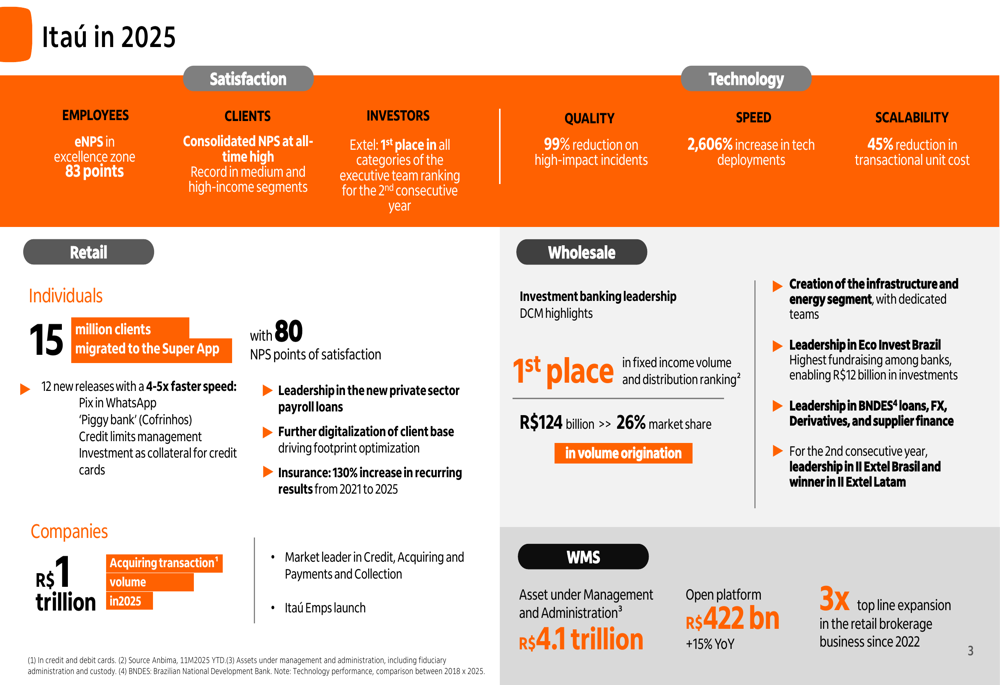

Itaú also showcased its achievements across various business segments in 2025, including technological advancements, customer satisfaction improvements, and market leadership positions:

Credit Quality & Portfolio Analysis

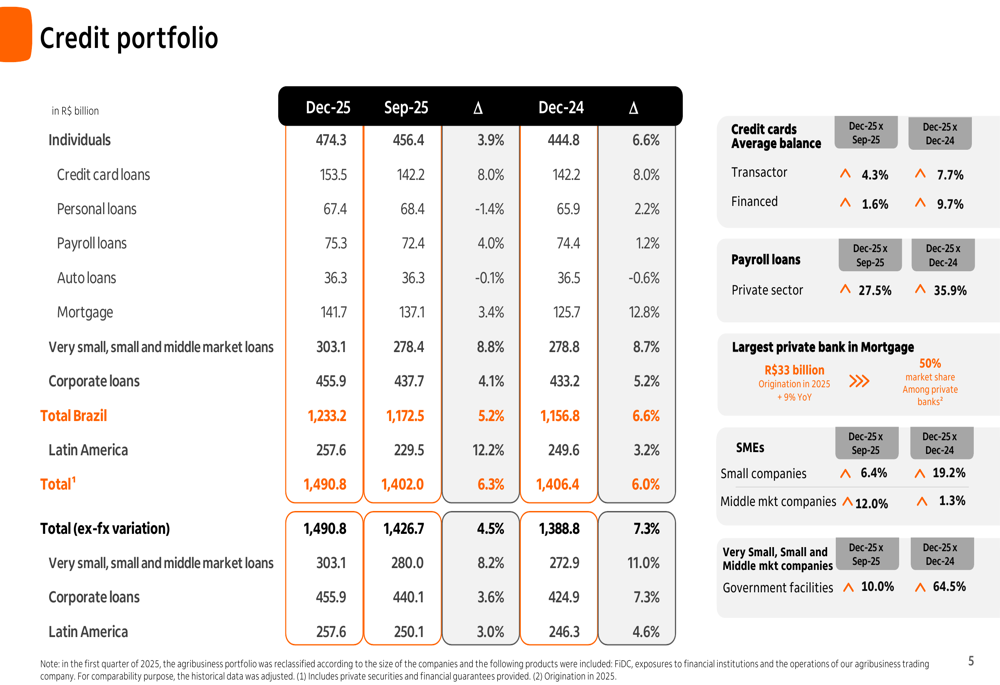

The presentation provided a detailed breakdown of Itaú’s credit portfolio, which reached R$1,490.8 billion by December 2025. Individual loans constituted R$474.3 billion, while corporate loans accounted for R$455.9 billion. The bank also maintained a significant presence in Latin America with a portfolio of R$257.6 billion.

The credit portfolio breakdown is illustrated in the following chart:

Credit quality metrics showed some signs of deterioration, with the 90-day NPL ratio in Brazil reaching 1.9% in December 2025. The individual segment reported a higher NPL ratio of 3.6%, while the corporate segment stood at 1.8%.

The cost of credit for Q4 2025 was R$9.4 billion, contributing to an annualized cost of credit to loan portfolio ratio of 2.5%. The bank’s renegotiated portfolio stood at R$35.1 billion in December 2025.

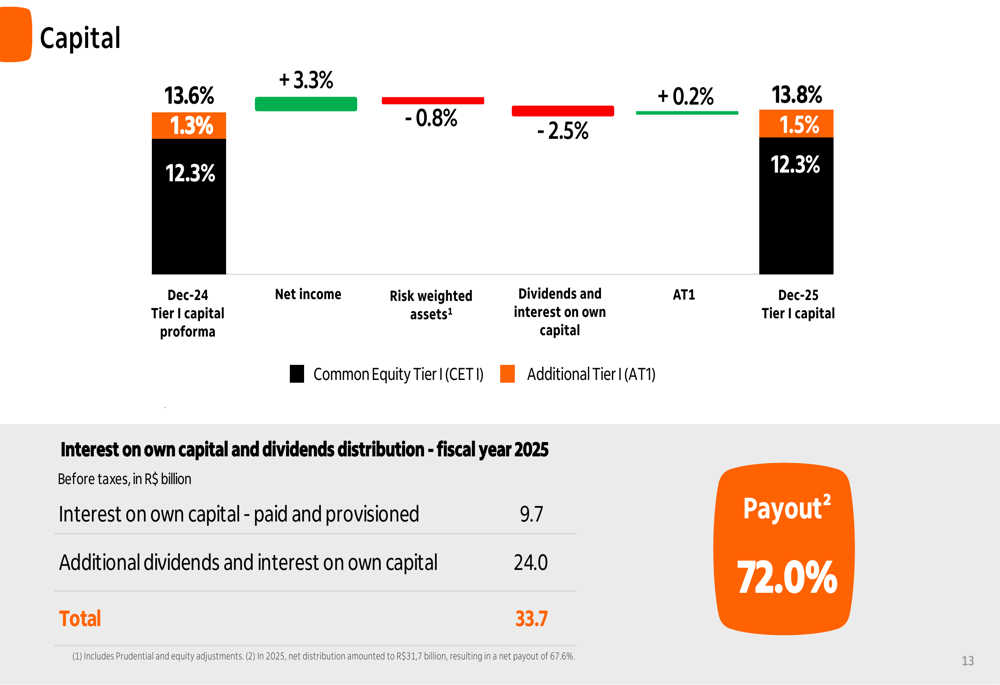

Capital Structure & Shareholder Returns

Itaú maintained a strong capital position while delivering significant returns to shareholders. For the 2025 fiscal year, the bank announced total dividends and interest on own capital of R$33.7 billion, representing a payout ratio of 72.0%.

The following chart details the bank’s capital structure and dividend distribution:

This generous shareholder return policy appears to have contributed to the positive market reaction despite the earnings miss, with the stock trading up in the premarket session.

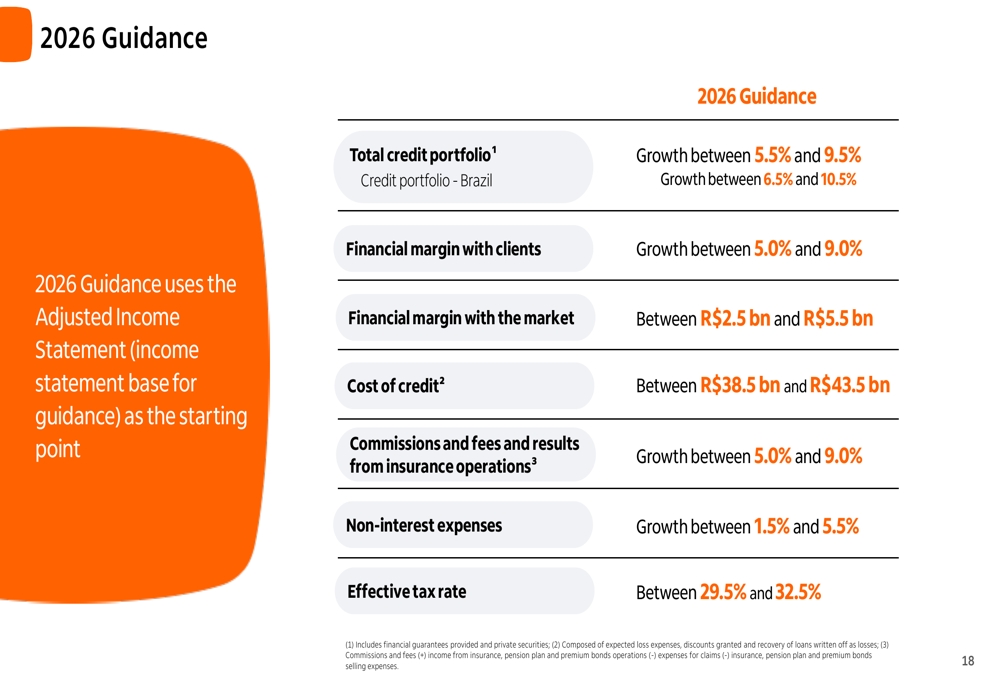

2026 Guidance & Outlook

Looking ahead to 2026, Itaú provided guidance across several key metrics, projecting continued growth albeit at a more moderate pace compared to 2025. The bank expects its total credit portfolio to grow between 5.5% and 9.5%, while financial margin with clients is projected to increase between 5.0% and 9.0%.

The complete 2026 guidance is presented in the following chart:

These projections are based on a macroeconomic outlook that anticipates Brazil’s GDP growth slowing to 1.9% in 2026 from 2.3% in 2025, along with a reduction in the SELIC rate from 15.00% to 12.75% by the end of 2026. Inflation is expected to moderate slightly to 4.0% in 2026 from 4.3% in 2025.

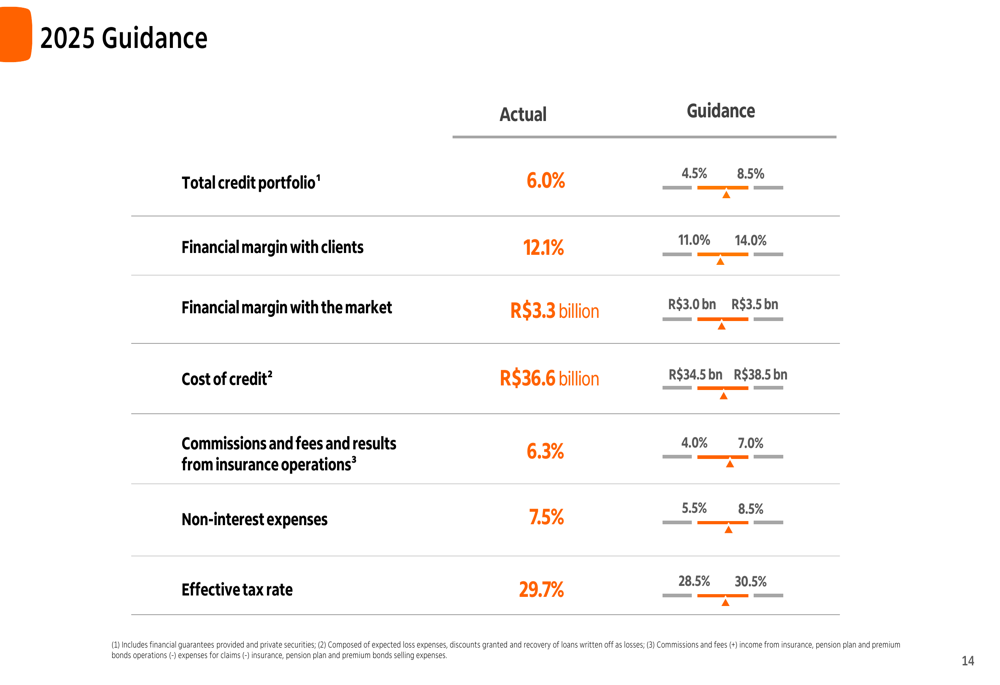

Performance Against 2025 Guidance

Itaú successfully met most of its 2025 guidance targets, with actual results falling within or exceeding the projected ranges for most metrics. The bank’s total credit portfolio growth of 6.0% fell within the guided range of 4.5% to 7.5%, while financial margin with clients growth of 12.1% exceeded the upper end of the 7.5% to 10.5% guidance range.

The comparison between 2025 guidance and actual results is illustrated in the following chart:

Despite the strong performance in local currency terms, the earnings article indicates that when converted to USD, Itaú’s revenue of $7.62 billion fell short of the forecasted $8.78 billion by 13.21%. This discrepancy highlights the impact of currency fluctuations on the bank’s reported results for international investors.

In conclusion, Itaú Unibanco’s Q4 2025 results demonstrate robust performance in local currency terms, with strong profitability, improved efficiency, and generous shareholder returns. While the bank missed USD-based analyst expectations, investors appear focused on the underlying operational strength and positive forward guidance, as evidenced by the stock’s positive premarket performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.